Friday, July 29, 2022

How can you measure the effects of inflation on your retirement savings?

Watch video on YouTube here: https://youtu.be/T6fudw4y-3M

Monday, July 25, 2022

The Recent Record High Inflation Numbers and The Impact Is having On Retirement

Why is Record High Inflation and The Impact Is having On Retirement accounts so scary?

Inflation can be scary because of its devastating effects on the purchasing power in a retirement savings account.

Let’s break this down by the numbers:

Most retirement planning prepares a retiree to live on their retirement savings for an average of 30 years. For easy numbers, let’s use a retiree who has saved $2M in their retirement account at the end of their working life.

Without considering inflation, this person could easily use the 4% rule by withdrawing $80,000 per year with a modest 2% return and still have $304,000 in their retirement account at the end of the 30 years.

If inflation is an average of 2% and returns are still 2%, and only withdrawing $80,000 without adjusting for inflation over retirement, the retiree would run out of money in 23 years. Right now, inflation is 9.8%.

If this pace of inflation were to persist over the next 30 years and the retirement account only grew by 2%, the retiree would take no withdrawals from the retirement account. At the end of the 30 years, the purchasing power inflation would have reduced the retirement account to $161,302!

Understanding the Inflation Numbers

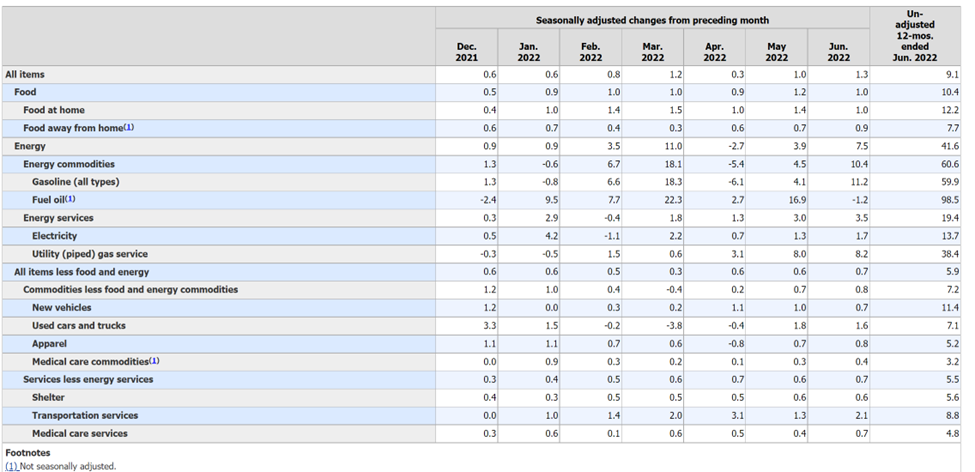

It’s good first to understand the current U.S. inflation numbers. As unadjusted, the inflation rate in the U.S. is increased by 1.3 % month over month, as this went just this month, June 2022, and has grown to a record year-over-year rate of 9.1 %. The U.S. Bureau Of Labor Statistics reports the U.S. inflation numbers.

The U.S. Bureau Of Labor Statistics takes market data and tracks a basket of commodity prices they deem necessary to consumers. The commodities include food, gasoline, energy prices, mortgage payments, new and used cars, and more. The average of prices each month is recorded and compared against the prior month’s and the subsequent year, providing the Consumer Price Index or CPI.

To see the latest BLS CPI number check out the BLS CPI site.

Some economists disagree with this method as commodities can be added or removed from the basket of goods based on how important the agency determines they are to the consumer at any given time. With a constantly changing basket of goods, deciding on the actual inflation rate can be challenging.

Looking at June’s Inflation numbers

As we look at the report in July showing June’s inflation numbers, we can see how the necessities such as food for home are above the 9.1% average. It costs families 10.4% to put food on the table at home over 1 year ago, which is a massive jump in food prices.

Individuals needing to travel for work are seeing an increase of 59.9% in Gasoline prices. It is reasonable to assert that the travel industry will eventually start seeing consumer spending habits change. Gas prices rise, and families feel the price hikes compared to a year earlier.

Inflation is called “The invisible Tax” due to its somewhat intangible effects on a savings portfolio. According to this BLS report, just to put some food on the table for you and your family this year compared to last, you need to have earned at least 10% more!

This 10% is just to break even. The slightly lower overall reported number of 9.1% is not much better.

An important question to ask is, when looking at your retirement portfolio, what was the average inflation rate used to calculate your retirement target?

Odds are it was a lot less than 6%.

source https://www.goldhillretreat.com/economy/inflation/record-high-inflation-impact-on-retirement/

Sunday, July 17, 2022

Saturday, July 16, 2022

What are the risks of inflation for retirees?

Watch video on YouTube here: https://youtu.be/fI4qTZnCKUY

Protecting Your Retirement: How to protect your retirement savings from inflation?

Watch video on YouTube here: https://youtu.be/kaQABq0Co_k

Monday, July 4, 2022

Are We Heading for a Recession What Economists are saying

Watch video on YouTube here: https://youtu.be/aB4KDxIdX4Y

Subscribe to:

Comments (Atom)

-

Are we in for a Global Recession? It’s a question on everyone’s mind: are we in for a global recession? And if so, what can we do to...

-

.jpg) 2022 Review of Augusta Precious Metals To learn more visit: https://www.goldhillretreat.com/inflation/hedge-against-inflation-with-augusta-...

2022 Review of Augusta Precious Metals To learn more visit: https://www.goldhillretreat.com/inflation/hedge-against-inflation-with-augusta-...